Stephen Z. Chundama and Ernest Nkrumah Addo

Sovereign debt has historically played a crucial role in providing emergency and development finance for budget support[1], monetary policy management, foreign reserves accumulation, and loan refinancing. However, debt accumulation often comes under scrutiny when low-income countries (LICs) experience widespread debt crises, such as the 1999 crisis that led to the Heavily Indebted Poor Countries (HIPC) Initiative. Experts argue that while debt itself is not inherently bad, its sustainability, transparency and responsible management are what matter.

Development of the LIC-DSF: An effort to provide a new solution to an old problem?

The Low-Income Country Debt Sustainability Framework (LIC-DSF) was introduced in 2005 to assess debt sustainability, set non-concessional borrowing limits and guide aid allocation. A review in 2017 aimed to enhance its relevance in the evolving global financial landscape, yet its core focus on public and publicly guaranteed (PPG) external debt remained unchanged.

As a result, the LIC-DSF has faced mounting criticism for its inability to prevent debt distress and major sovereign debt crises. Today, with 21 African countries either in or at high risk of debt distress, the effectiveness of the LIC-DSF is once again under scrutiny.

Has the LIC-DSF helped to prevent major debt crises?

Numerous experts, including Brian Pinto (2018) and Indermit Gill (2024), have argued that the LIC-DSF has become obsolete and ineffective in preventing sovereign debt crises. Despite multiple reviews intended to enhance its relevance, the number of LICs at risk of debt distress has remained persistently high.

While external factors such as the Global Financial Crisis (2007–2008), the COVID-19 pandemic (2019–2023), and the ongoing Russia-Ukraine war (2022–present) have undoubtedly exacerbated debt vulnerabilities, the framework's shortcomings are evident.

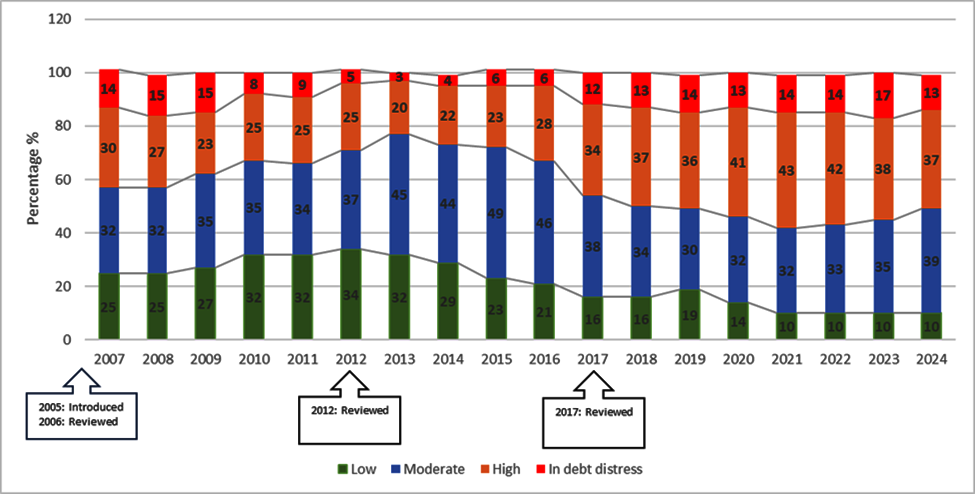

Figure 1: Low Income Countries Debt Sustainability Profile (2007 – 2024)

Source: Authors’ Calculations using IMF (2024) & UNDESA (2024)

As seen in Figure 1, since 2013, the number of LICs in or at high risk of debt distress has been steadily increasing, despite comprehensive reviews of the LIC-DSF in 2012 and 2017.

Why has the LIC-DSF failed?

The IMF asserts that Debt Sustainability Assessments (DSAs) should not be interpreted rigidly but should consider country-specific circumstances. However, this contradicts the LIC-DSF’s mechanistic nature, as it relies on static debt burden thresholds and benchmarks. Expecting dynamic analysis from a static framework is unrealistic.

Furthermore, the IMF plays a central role in setting macroeconomic parameters for countries in its programs and advising governments on external debt management through its Article IV consultations. This means the IMF is well aware of the unique circumstances these countries face. However, the LIC-DSF fails to adequately capture these realities, leading to repeated underestimation of debt sustainability risks – as seen when it failed to foresee the severity of the COVID-19-induced recession.

Most of the weaknesses of the LIC-DSF are well summarized in the sharp critique by Brian Pinto (2018). These include the LIC-DSF’s:

1. Obsolete focus on PPG external debt – The unsatisfactory incorporation of total public debt by simply grafting domestic debt onto the present value of external public debt introduces inaccuracies associated with the choice of discount factor and confuses the symptoms with the malady.

2. Failure to integrate market signals – Designed for an era dominated by concessional financing, the framework has not adapted to the growing role of non-concessional debt. Of the total sources of sovereign debt, private lenders (including bondholders) have increased their share from 9% in 2000 to 25% at the start of 2023. Within the same period, Paris Club lenders reduced their share from 39% to 10%.

3. Lack of alignment with the Sustainable Development Goals (SDG’s) – The LIC-DSF does not reconcile debt sustainability with long-term development objectives.

4. Inadequate early warning indicators – The framework has failed to provide timely alerts of impending debt crises.

Is the LIC-DSF solely to blame?

These stark weaknesses beg the question: should the ongoing sovereign debt crisis be solely attributed to the failure of the LIC-DSF? Certainly not. Sovereign debt distress is a function of numerous factors including a country’s legislative framework and oversight, governance systems, domestic resource mobilization capacity, efficiency of spending, credibility of domestic macroeconomic policies, availability of concessional finance, and exposure to global economic shocks e.g. commodity price shocks, to mention a few.

One may also ask: could a dynamic, responsive and representative DSF have helped to prevent the current crisis? The answer to that question is indeterminate. What is certain, however, is that the current LIC-DSF was completely ineffective in providing early warning of a pending crisis since the insights it provided were not much better than what the simple Debt-to-GDP ratio showed.

In conclusion, the current LIC-DSF should be completely discarded and replaced with a new, dynamic, realistic and responsive DSF that reflects the times we live in – not symbolic, cosmetic fixes through arbitrary reviews that merely give a false appearance of remedial action being taken. Ultimately, as stated in the UN General Assembly resolution 75/153, individual countries remain responsible for their debt sustainability.

Disclaimer: The views expressed in this article are solely attributed to the authors.

[1] Sovereign debt has historically been used to support budgets for infrastructure development, social services, climate change adaptation, technology and Innovation etc.